Figures are estimates; your offer may differ based on checks and fees.

Clear monthly payment

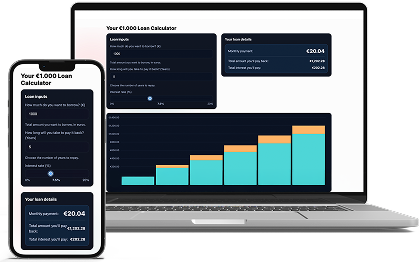

See principal vs. interest over time and plan an affordable budget.

Flexible terms

Shorten the term to cut interest — extend it to lower the monthly cost.

Built for speed

Simple, responsive, accessible. No clutter — just the numbers you need.

FAQ: Loan Cost Estimate Calculator

It uses the standard fixed-payment (amortizing) method that banks use, matching your annual rate and term to monthly payments. Each payment covers interest first, with the remainder reducing principal.

Interest is charged on the remaining balance, which is largest at the start. As the balance falls, the interest slice shrinks and more of each payment goes to principal.

The interest rate is the nominal yearly price of the loan. APR (for loans) and APY (for savings) are effective yearly measures that account for compounding and, for APR, sometimes certain fees.

No. Results show the core loan mechanics (principal, rate, time). Add lender fees, taxes, or insurance separately, since they vary by product and location.

The baseline view assumes the standard schedule. Extra principal payments shorten the term and reduce total interest — we can add an “extra monthly” input if you want it built in.

A cumulative view makes progress crystal clear — you see total principal repaid and total interest paid grow over time, with early years interest-heavy and later years principal-heavy.

Yes, in reverse: contributions and interest are added each period, so you earn interest on a growing amount. The chart stacks contributions and interest to separate your input from growth.